LONDON- Chicago-based United Airlines (UA) has emerged as the top carrier for Europe-US flights in July 2024, based on available seats.

This marks a shift from pre-pandemic rankings when Delta Air Lines (DL) held the leading position. AIR SERVICE ONE’s analysis of Cirium data by Ralph Anker reveals significant changes in the transatlantic air travel market.

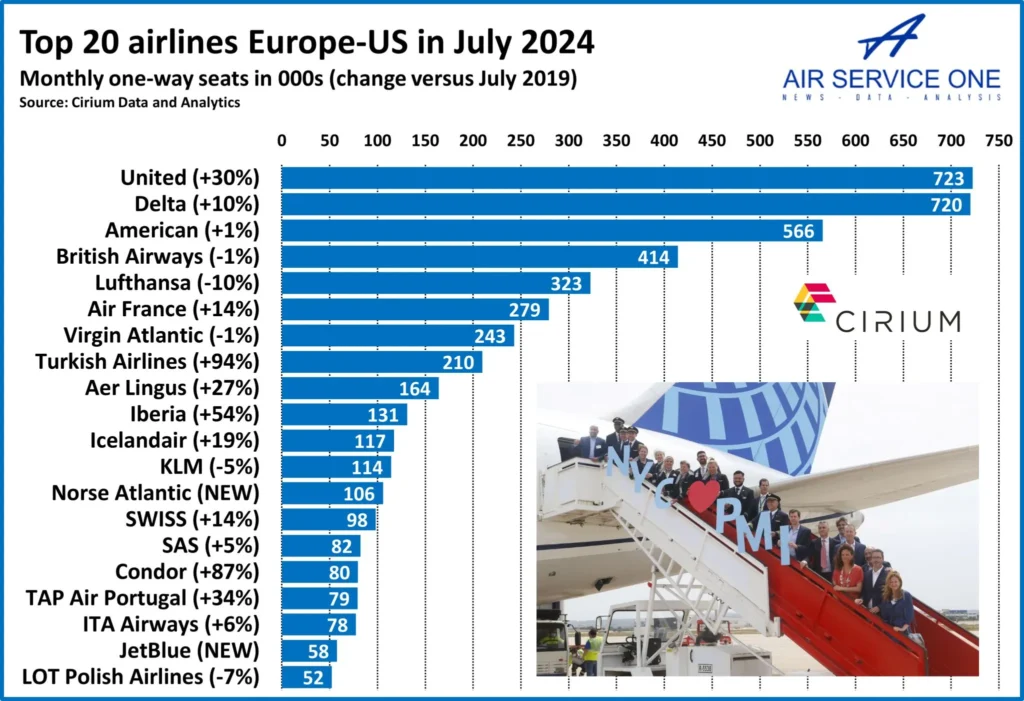

United Leads Europe-US Routes

United Airlines has shown remarkable growth, increasing its capacity by 30% compared to July 2019, offering 723,000 monthly one-way seats. Delta follows closely with 720,000 seats, representing a 10% increase. American Airlines (AA) rounds out the top three with 566,000 seats, showing a modest 1% growth.

The data reveals interesting trends among European carriers. British Airways (BA) and Virgin Atlantic (VS) have maintained relatively stable capacities, with only a 1% decrease each. Lufthansa (LH), however, shows a 10% reduction in seats, indicating a more cautious approach to recovery.

In contrast, Air France (AF) has expanded its offerings by 14%, suggesting a more aggressive strategy for capturing transatlantic market share.

Turkish Airlines (TK) emerges as the standout performer among European carriers, with a staggering 94% increase in capacity. This dramatic growth positions Turkish Airlines as a major player in the Europe-US market, potentially reshaping competitive dynamics.

New Entrants

The transatlantic market has also welcomed new entrants. Norse Atlantic Airways (N0), a newcomer to the scene, has quickly established itself in the top 15, offering 106,000 seats.

JetBlue (B6), known primarily for its domestic US operations, has also made its debut in the transatlantic market, securing a place in the top 20 with 58,000 seats.

Other European carriers showing significant growth include Aer Lingus (+27%), Condor (87%), Iberia (+54%), and TAP Air Portugal (+34%). These increases suggest a strong recovery and expansion strategy among these airlines, potentially capitalizing on pent-up demand and new market opportunities.

The data also highlights the challenges faced by some carriers. KLM (KL) shows a 5% decrease in capacity, while LOT Polish Airlines (LO) has reduced its offerings by 7%.

These figures indicate that recovery and growth are not uniform across the industry, with some airlines still navigating challenges in the post-pandemic landscape.

Interestingly, the overall increase in seats (5.5%) is outpaced by the increase in flights (8.8%), pointing to a trend towards the use of smaller aircraft on transatlantic routes. This shift could be driven by factors such as operational flexibility, fuel efficiency, or changes in demand patterns.

Some Quit After the Pandemic

The absence of Norwegian (DU and DI) from the top ranks, previously a significant player in the low-cost long-haul market, marks a notable change in the competitive landscape.

Similarly, the exit of Thomas Cook Airlines (MT) and Aeroflot (SU) from this market underscores the significant restructuring that has occurred in the wake of the pandemic and geopolitical shifts.

With new players entering the market, established carriers adjusting their strategies, and overall capacity rising, passengers can expect a diverse range of options for their Europe-US travel plans in the summer of 2024.

Stay tuned with us. Further, follow us on social media for the latest updates.

Join us on Telegram Group for the Latest Aviation Updates. Subsequently, follow us on Google News.